PHOTO

First-home buyers are borrowing larger amounts while putting down smaller deposits as they take advantage of government housing schemes, while a separate debate is intensifying over the cost of tax concessions for property investors and their impact on inequality in home ownership.

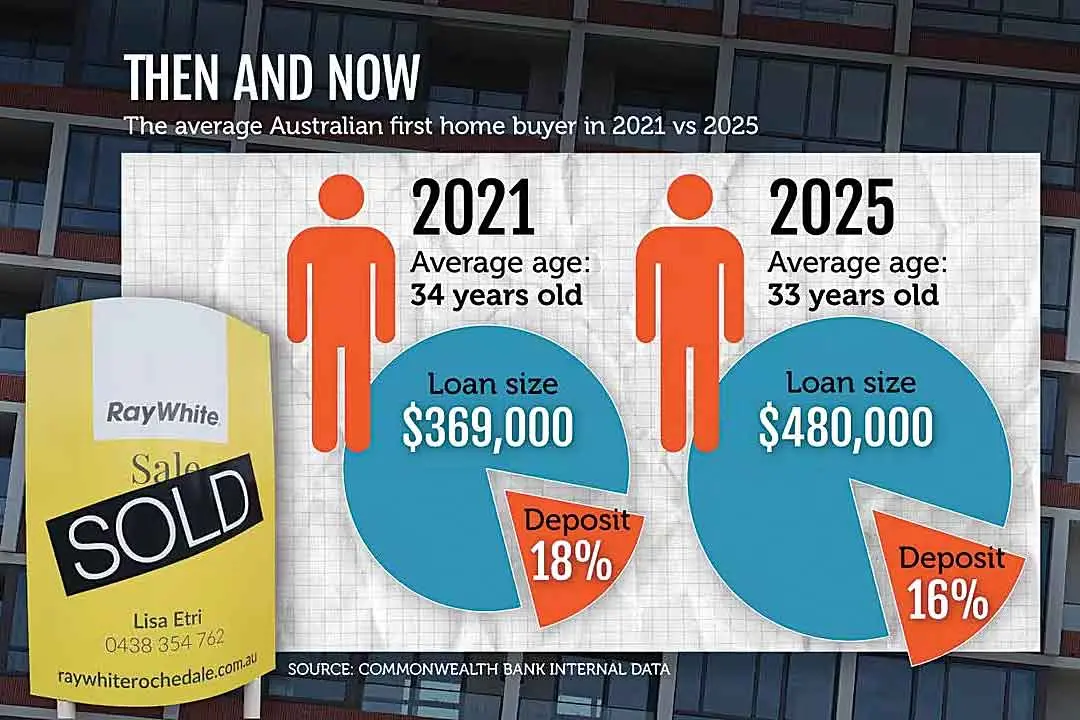

Borrowing patterns of first homebuyers are changing as they take advantage of government subsidies, according to Australia’s biggest lender, the Commonwealth Bank.

The bank’s internal data shows the average first-home buyer in 2025 borrowed $480,000, up from $369,000 in 2021. At the same time, the typical deposit has fallen to 16 per cent, down from 18 per cent in 2021.

“More of our customers are taking advantage of government schemes that help them buy sooner, without the cost of lenders mortgage insurance,” Commonwealth Bank home buying general manager Rebecca Markwell said.

Since July 2022, nearly 50,000 CommBank customers have used the federal government’s five per cent Deposit Scheme to buy a home.

The scheme allows eligible buyers to purchase a property with a smaller deposit without paying lenders mortgage insurance. The federal government expanded the program in October 2025, removing income caps and making it available to an unlimited number of applicants.

The data also shows most first-home buyers are still purchasing in cities. Almost three-quarters of first-home buyers in 2025 purchased in metropolitan areas, a trend that has remained steady since 2021.

Homebuyers purchasing in metropolitan areas took out an average loan of $507,000, compared with $400,000 for those buying in regional or remote areas.

“Some want to stay close to the opportunities and connectivity that come with metropolitan living, while others are looking to more regional areas where they could secure a larger property at a more accessible price point,” Ms Markwell said.

In NSW, the city of Orange in the Central Tablelands was the most popular location for the bank’s first-home buyers in 2025. Other hotspots included Tarneit in western Melbourne, Greenbank in Queensland, Mount Barker in South Australia, Baldivis in Western Australia, Claremont in Tasmania, Zuccoli in the Northern Territory and Belconnen in the ACT.

Separate data from housing analytics firm Cotality shows that in some areas mortgage payments for an apartment are now about the same as, or even cheaper than, renting.

The result reflects the speed at which rents have surged, with the national index up 5.5 per cent over the year, compared with more moderate gains in unit values. However, the analysis does not include other costs of ownership, such as deposits, council rates, insurance, body corporate fees and maintenance. Detached houses remain significantly more expensive to purchase than rent across capital city regions.

While policies designed to assist first-home buyers have expanded, a separate housing debate is focusing on tax concessions for property investors and their impact on the federal budget.

Research published by the Parliamentary Budget Office on Friday estimated the capital gains tax discount and negative gearing deductions on investment properties could cost taxpayers more than $24 billion per year by 2035-36.

The analysis was commissioned by the Greens, whose treasury spokesman Nick McKim is leading a Senate inquiry into the capital gains tax discount.

“Winding back the CGT discount would help renters, first-home buyers and the budget,” Senator McKim said. “The evidence given to the Greens-led Senate inquiry has made the case for change overwhelming.”

The Parliamentary Budget Office found the two tax concessions together would result in $15.4 billion in forgone revenue this financial year. Since 2015-16, almost $110 billion has been forgone, with another $190 billion expected over the next decade.

Analysis released by the Australian Council of Social Service found 22 per cent of all capital gains tax discount expenditure accrued to Australia’s five wealthiest electorates, all located in Sydney and Melbourne.

“This is money that could be invested in social housing, essential services, income support and the communities that need support the most,” ACOSS chief executive Cassandra Goldie said. “Instead, it's being used to supercharge inequality.”

However, some economists argue reforming the concession may not raise as much revenue as advocates expect.

Peter Tulip, chief economist at the Centre for Independent Studies, said investors would likely change their behaviour in response to new tax settings, prioritising other assets or delaying sales to avoid realising gains.